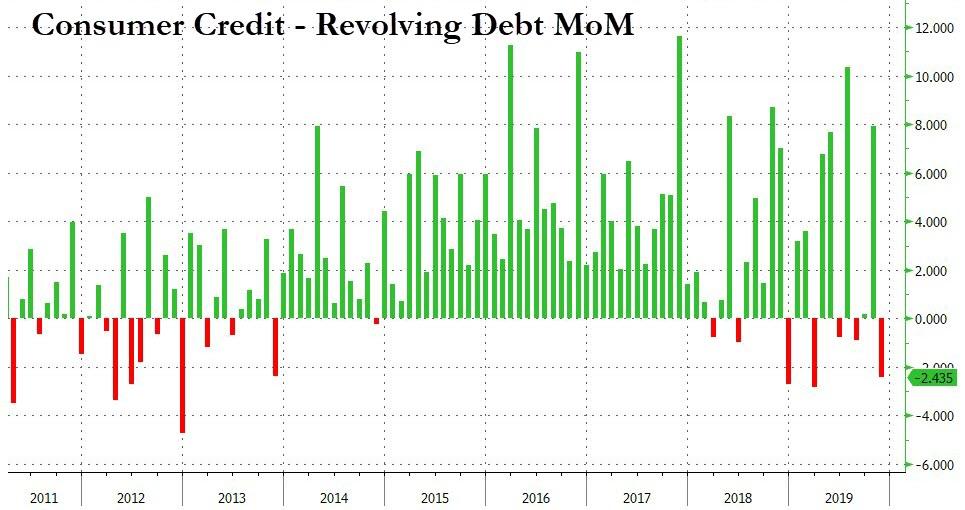

One month after the burst in credit card usage, when in October revolving, i.e., credit card debt soared by $7.9BN or the most since July, in November US consumers hunkered down and just as the holiday spending was in full force, and unexpectedly repaid $2.4BN in credit card debt, the most since March, bringing the total credit card debt outstanding to $1.086 trillion, just shy of the record hit in October.

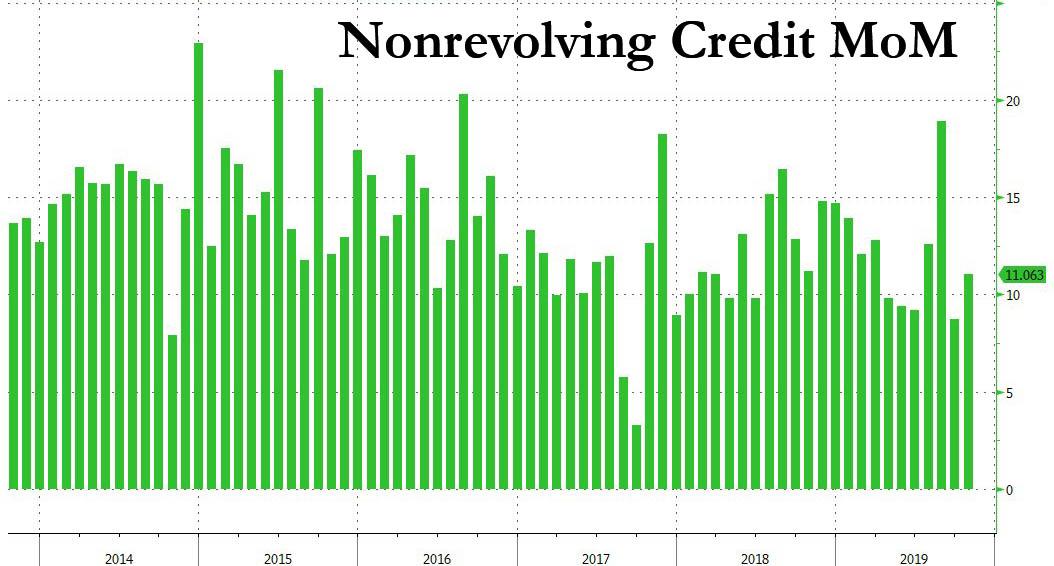

Offsetting this drop, was another surge in non-revolving debt, i.e., student and auto loans, which rose by $14.9BN, the biggest monthly increase in four months, and the second highest monthly increase since August 2018.

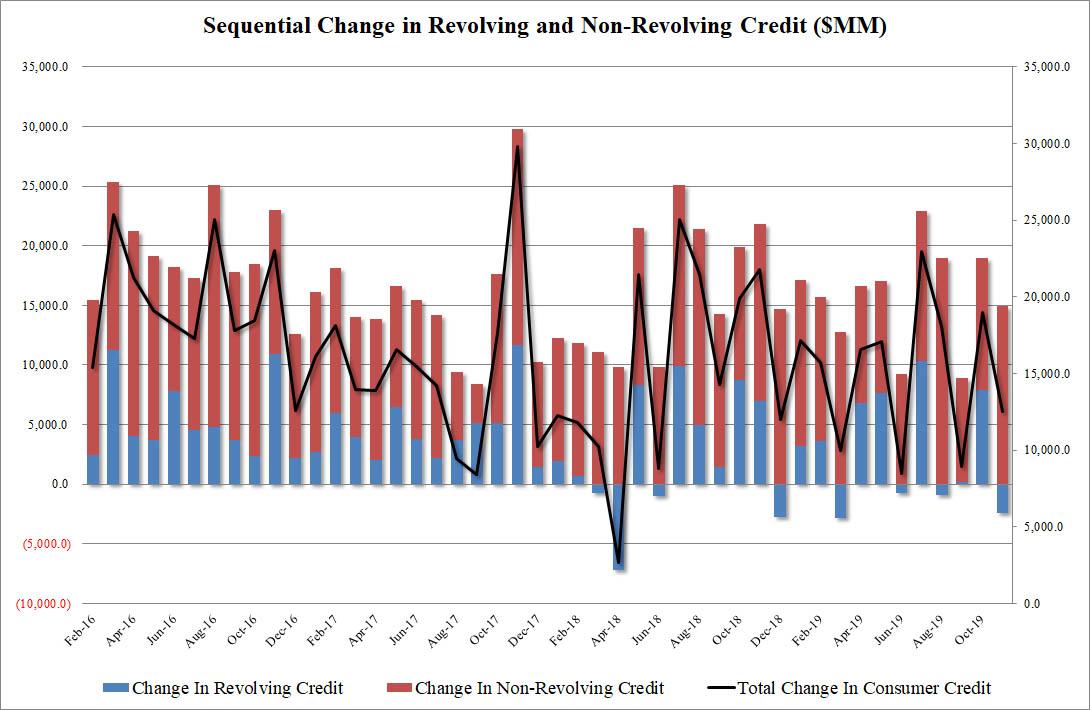

Combined, November's total increase in consumer credit was $12.5BN, which was below October's massive $19BN, and below the consensus estimate $16BN, entirely on the back of the unexpectedly drop in credit card debt.

Considering the strong end to the year for retail sales, especially online, we assume this was a one-off event, and in December any credit card "shrinkage" was more than offset with aggressive year-end "charging." If not, then the US consumer may indeed be reaching the limits of their debt-funded spending euphoria.

Tyler Durden Wed, 01/08/2020 - 15:17 Tags Business Finance{kind=link}

{kind=link}

{kind=link}